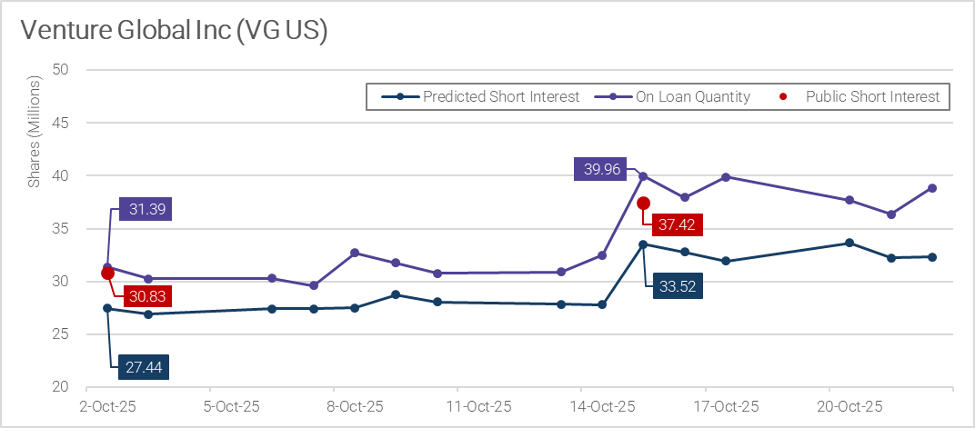

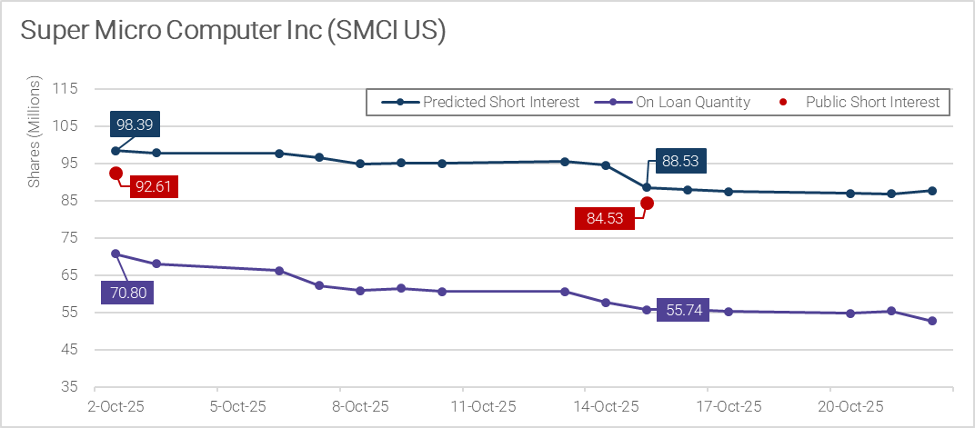

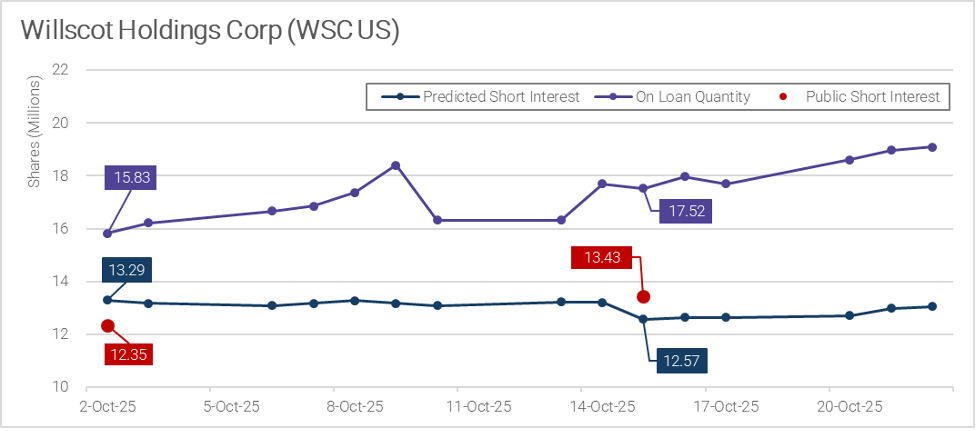

Predicted Short Interest: A New Lens on Market Positioning

Understanding short interest is critical, yet traditional short interest data has significant...

Read More

2025: The Year AI Reshaped the Lending Landscape

2025 was a defining year for AI-linked equities. Markets aggressively rewarded companies...

Read More